On 12 June 2026, SpaceX became a public company. It priced at 135 dollars, opened at 150, closed its first day up 19 percent, and raised roughly 75 billion dollars at an implied valuation near 1.77 trillion. It is the largest initial public offering in history, and for the next several months it will be the single most discussed line item in family-office and allocator conversations everywhere.

So this is a useful moment to be precise about something the industry says loosely all the time: that technology IPOs deliver strong returns. They do, on average. The trouble is that nobody can buy the average. You can buy a fund, or you can buy a stock, and the data on what those actually returned tells a much harder story than the headline does. We can be precise because we hold the data: our private-capital database spans more than 3,700 fund-level performance records and quarterly returns back to 1996.

A word on the data: the fund-return analysis is computed on our proprietary private-capital database and verified against our live data. The SpaceX listing facts and the comparable-IPO returns are publicly reported and labelled as estimates; the lock-up mechanics are inference from published academic research. This is research, not investment advice, and SpaceX is a worked example, not a recommendation.

01 · The power law

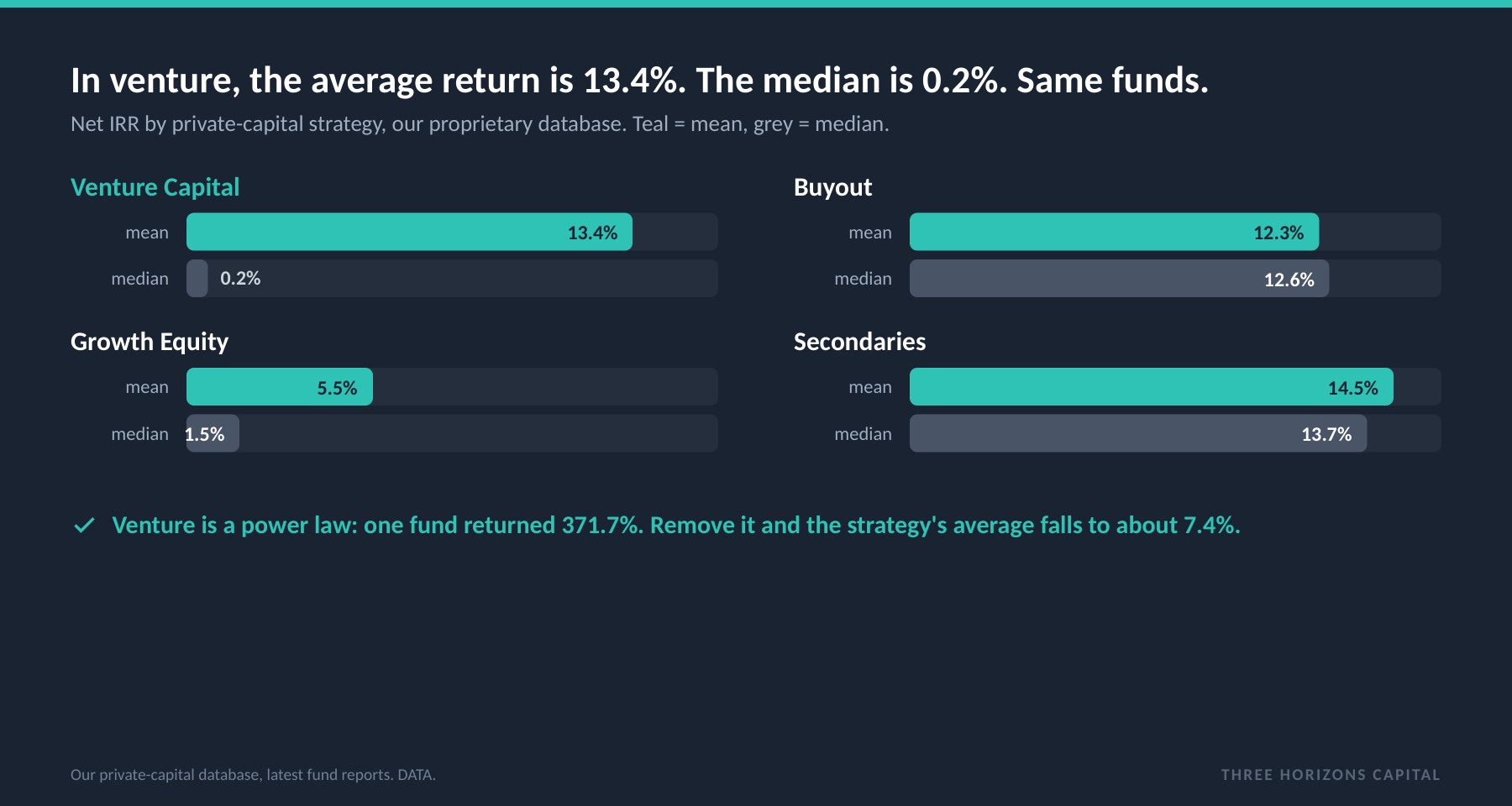

The average is an illusion. The median tells the truth.

Across the venture funds in our database, the mean net internal rate of return is 13.4 percent. The median is 0.2 percent. These two numbers describe the same universe of funds, and the gap between them is the entire argument against buying tech-IPO hype as an asset class.

What this tells you: Venture returns are a power law, not a bell curve. The single best fund in our venture universe returned 371.7 percent net; remove it and the strategy's average falls to roughly 7.4 percent. Half of all venture funds returned less than 0.2 percent. Gaining exposure to venture, or to tech IPOs, as an asset class is not the same as capturing the returns that justify the headline. Those returns come from selection, not exposure.

02 · Vintage

Vintage beats conviction.

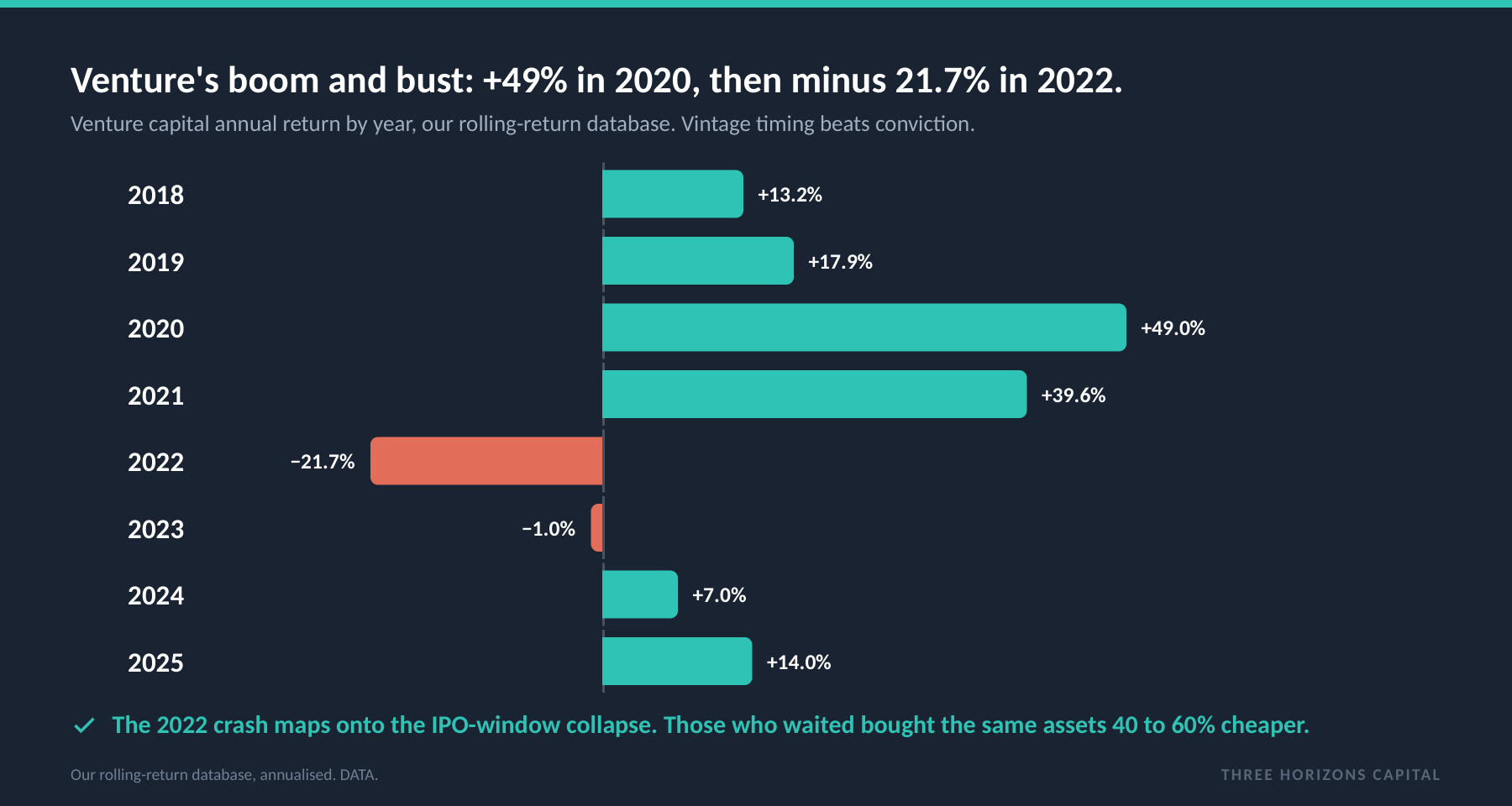

When you enter matters more than how much you believe. Venture is the most volatile strategy in private markets by a wide margin, and the recent cycle makes the point without commentary.

Venture returned +49.0 percent in 2020 and +39.6 percent in 2021, then −21.7 percent in 2022, a correction that maps almost exactly onto the collapse of the IPO window, the period of Rivian and WeWork. Investors who chased venture-backed IPOs at the peak bought the top and lived through the correction before any recovery. Those who entered afterward bought the same assets at 40 to 60 percent discounts. For a family office sizing a single high-profile position, vintage matters more than conviction.

03 · The lock-up clock

The structural variable is a date on the calendar.

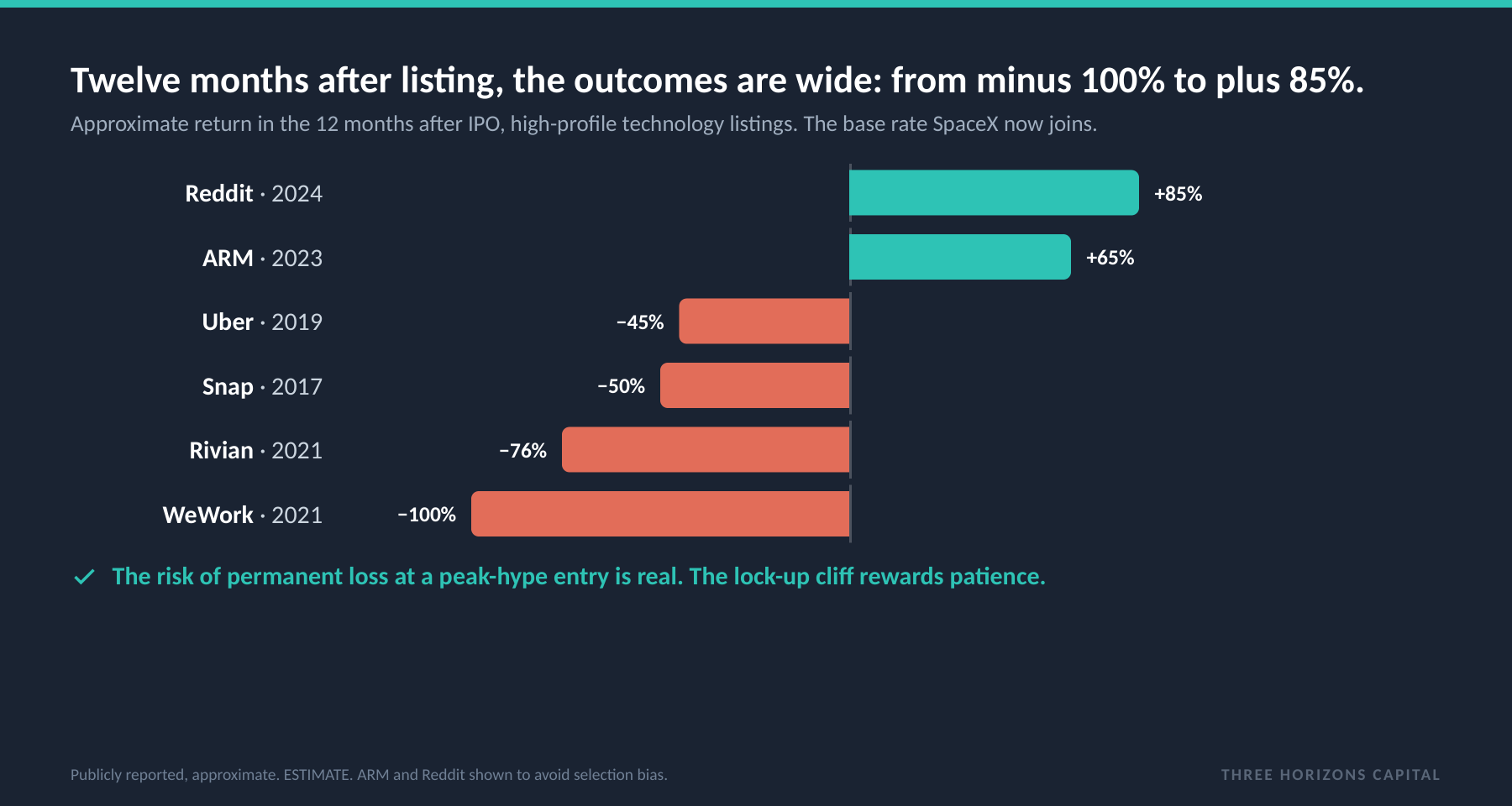

For anyone who did not own SpaceX before the listing, the question is not whether to admire the company. It is how a new listing behaves. On IPO day only a slice of the shares trade, typically 10 to 20 percent, and that scarcity supports and often inflates the opening price. SpaceX has already had that pop. The more important date comes later: the standard 180-day lock-up expires around Month 6, releasing insider shares on a single predictable date. For SpaceX, the cliff lands around December 2026.

The comparable base rate, twelve months after listing, should be read without selection bias: Rivian fell 76 percent, Snap 50 percent, Uber 45 percent and WeWork went to zero, while ARM rose 65 percent and Reddit 85 percent. The distribution of outcomes is wide and the risk of permanent loss at a peak-hype entry is real. The point is not that famous IPOs fail. It is that the lock-up cliff hands a patient buyer a structurally better entry than IPO day offered.

04 · SpaceX

SpaceX is three bets the market is now pricing as one.

SpaceX operates three structurally different businesses, and the market must price all three at once: Starlink broadband (the recurring-subscription engine of last year's roughly 18.7 billion dollars of revenue), launch services (mature in Falcon 9, early in Starship), and the longer-dated space economy (largely conceptual and decades from revenue). At roughly 1.77 trillion dollars, the listing prices in success across all three simultaneously. Each assumption is plausible in isolation; requiring all of them to be correct at once, at that valuation, is the kind of bet that historical tech-IPO valuations have rarely rewarded at peak enthusiasm. At this scale SpaceX also becomes one of the largest listed companies in the world, forcing buying from passive index funds regardless of fundamentals, which can support an elevated price longer than analysis would suggest, then unwind quickly if growth disappoints.

The honest part: Early venture investors built positions at a cost basis a fraction of today's, an advantage that is not recoverable. A post-IPO buyer should not try to replicate a venture return profile. The right frame today is a liquid-equity investment in a well-defined, very richly valued technology company, with all the discipline that implies, not a venture bet on a startup.

05 · The discipline

The discipline is the protection, not the asset.

The families most harmed by past hype cycles shared one trait: they sized the position as a statement of conviction rather than a disciplined allocation. The quality of the asset is secondary to the quality of the process, and the process is simple to state and hard to follow. Size it before you are excited, with a hard cap near 3 to 5 percent of assets written down first. Audit the technology beta you already hold, because a famous name on top of a growth-heavy book is correlated risk, not diversification. Let the Month-6 lock-up clock work for you as an entry window rather than chasing the pop. And decide how you lose before you decide how you win.

None of this requires a view on whether SpaceX succeeds. It requires a view on how a portfolio should hold a position whose range of outcomes is genuinely wide. The lesson is portable on both sides of the table. If you allocate, count the base rate, not the headline. If you advise those who do, the same analysis is a conversation you can open with evidence rather than enthusiasm.

The fund-return figures are verified against our own database. The SpaceX listing facts and comparable-IPO returns are publicly reported estimates; the lock-up underperformance ranges are inference from academic research. This is research, not investment advice, and SpaceX is a worked example, not a recommendation.

Sources: Three Horizons Capital proprietary private-capital database (fund-level net IRR and TVPI; quarterly rolling returns 1996 to Q3 2025), verified against our live data; SpaceX listing facts and comparable-IPO returns from publicly reported data as of 28 June 2026; lock-up underperformance from published academic research. For research and platform-demonstration purposes; not investment advice.