On 17 June 2026, Federal Reserve Chair Kevin Warsh held his first meeting and changed the weather. Rates stayed at 3.50% to 3.75%, but the message did not stay still: the committee removed its bias toward cuts, the median projection moved toward at least one more hike this year, and easing was pushed out to 2027 and beyond. The cause is an inflation the Fed cannot fix with rate policy, because it is coming from the price of energy in a year of conflict. CPI reached 4.2% in May, the highest reading since April 2023.

For a family office, the instinct is to reach for the familiar rates-and-bonds checklist: shorten duration, trim the long end, move on. That checklist looks in the wrong place. The real rate risk in a modern, growth-tilted, illiquid-heavy portfolio is not sitting in the bond sleeve. It is hidden inside private equity, real estate and public equities, and the standard risk model cannot see it.

A word on the data: portfolio analytics are computed on J.P. Morgan's 2026 Long-Term Capital Market Assumptions (10-year, USD). We verified the asset-class baselines this analysis depends on against our own LTCMA data, and they match to the basis point. The factor decomposition, scenario results and rate-sensitivity spectrum are model-derived estimates, labelled as such throughout. The macro backdrop (the June FOMC, May CPI) is corroborated against public reporting. The reference portfolio is analytically constructed and is not based on any client's holdings. For research and platform-demonstration purposes; not investment advice.

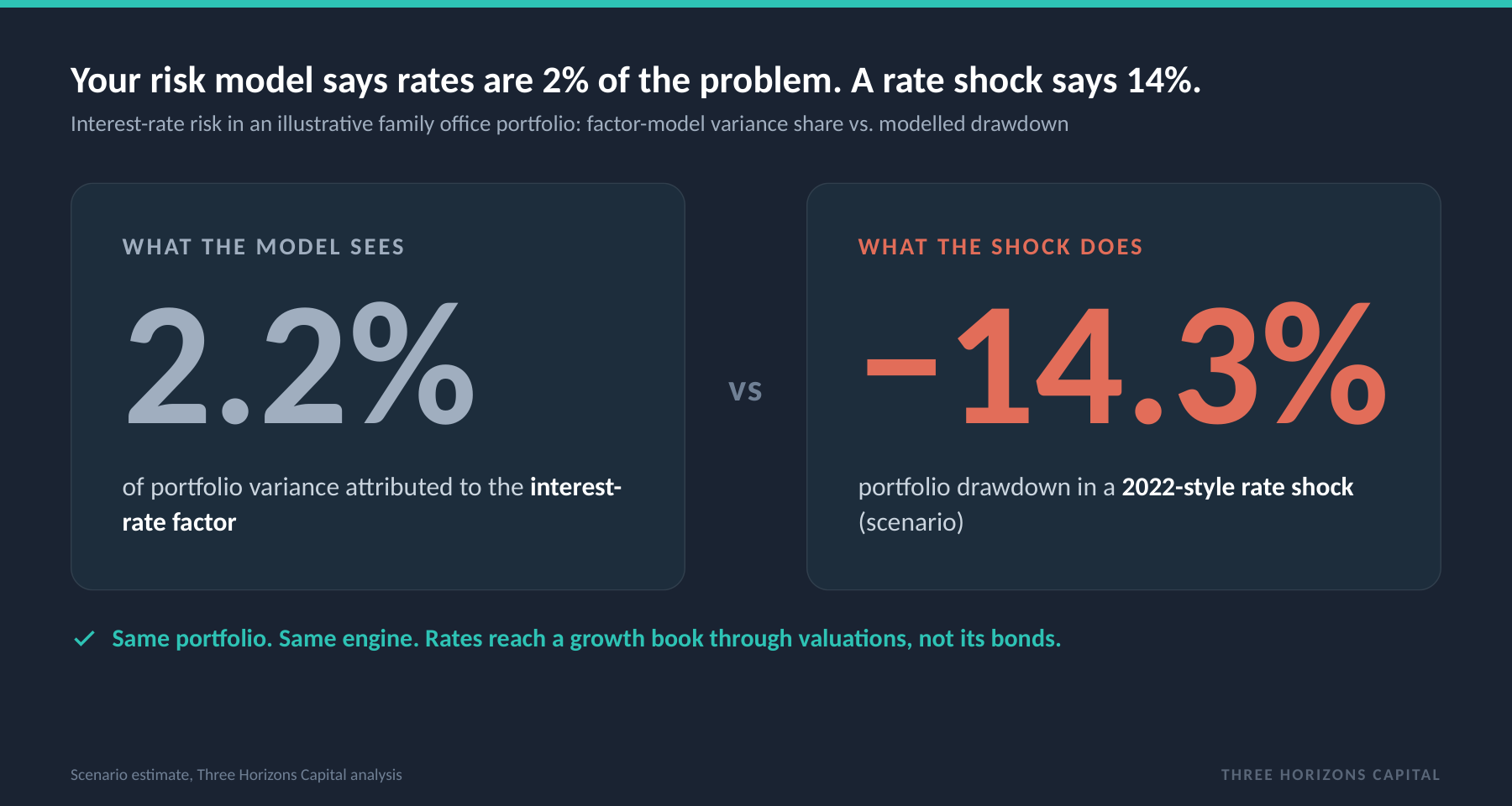

01 · The reassuring number

Two percent of the risk. Fourteen percent of the drawdown.

Run a formal three-factor model over the portfolio and it attributes 2.21% of variance to the interest-rate factor. On paper, rates are a rounding error. Stress the same portfolio with a shock on the scale of 2022 and it returns a 14.3% drawdown, larger than the loss it projects for a normal recession. Both numbers come out of the same engine.

What this tells you: A factor model measures statistical co-movement between holdings and rate-proxy instruments, mostly bonds. It is close to blind to the way rates reach a growth portfolio, which is through valuation. It is blinder still for concentration: this book holds twelve nominal positions but behaves like 4.1 effective positions, because its assets move together. Risk that looks spread across a dozen line items is, underneath, a few correlated bets, and rates move several at once.

02 · The transmission

Rates do not arrive through the bonds. They arrive through valuations.

Rate risk reaches this portfolio through three valuation channels, none of which runs through the bond allocation the model is watching. Each conceals the loss in a different way.

Private equity, 22% of the book, through the discount rate

The largest single holding. A higher discount rate compresses the value of distant cash flows most. Marks lag reality by one to three quarters, so the first risk report after a shock looks calm while the loss has already happened.

Core real estate, 9% of the book, through the cap rate

The highest rate sensitivity per dollar of any holding. Rising rates lift cap rates mechanically and compress values. Quarterly appraisal crystallises the loss slowly, so low reported volatility is delayed information, not safety.

Public equities, ~32% of the book, through the multiple

Higher rates raise the discount rate on future earnings and make bond yields compete with the equity risk premium. Today's richer starting valuations amplify the contraction.

Add the channels up and the 14.3% stops looking surprising. The model was not wrong about the bonds. It was silent about everything else.

03 · The broken hedge

A slowdown no longer buys you a rate cut.

For most of the last fifteen years, a slowdown was its own insurance: growth wobbled, the Fed cut, yields fell, and falling yields cushioned the equity loss. Stocks and rates offset each other. The current regime breaks the reflex. When inflation is the binding constraint, a mild slowdown does not automatically buy a rate cut, so the portfolio can face growth risk and rate risk at the same time, with no monetary relief to net them off. That is why the scenario model puts the rate shock, not the recession, at the top of the risk ranking for this environment.

Even the single hike the market is now weighing produces an estimated 2.4% at the portfolio level. The relationship is roughly linear for small moves and turns non-linear at the extremes, as forced selling and lagged marks amplify the theoretical transmission.

04 · The fix

Buy resilience, do not sell growth.

The fix is not a defensive crouch. The portfolio's 7.07% expected return comes from its growth and illiquidity, and none of that need be surrendered. The problem is narrower: the natural hedge budget, at 12% of assets, is too small for the rate environment. Five targeted adjustments close most of the gap, each funded from within the book: add TIPS (0 to 4%), expand direct lending (5 to 8%), initiate macro hedge funds (0 to 3%), trim core real estate (9 to 5%), and double gold (2 to 4%).

The funding chain is shown illustratively. The modelled rate-resilient portfolio is normalised to 100% of assets, with the gold increase funded partly from the real estate trim and partly from a small trim elsewhere.

What this tells you: The Bond Shock drawdown improves from −14.3% to −12.7%, a gain of 160 basis points, while expected return falls by 8 basis points and volatility falls by 42. The natural hedge budget rises from 12% to 21% of assets, and effective positions improve from 4.1 to 4.8. A Sharpe ratio that moves by 0.007 is inside the model's own noise. That is roughly twenty to one, on the risk most relevant to the current policy environment.

05 · The risk you cannot model

The honesty is the point, not the footnote.

Two risks sit outside any scenario table, and pretending otherwise is its own error. The first is the governance gap inside private equity: because marks lag, reported volatility in the first quarter of a rate shock can understate the true drawdown by an estimated 300 to 600 basis points. Risk reports written in that window are not a safe basis for positioning; capital-call planning must assume the full economic hit before the marks show it; and any apparent private-market outperformance during the shock is an accounting artefact, not skill.

The second is the redesign of Fed communication itself. The Chair has signalled a review of how the committee guides markets, including the dot plot that has anchored forward rate pricing since 2012. If that anchor is widened into ranges, published less often, or retired, the credible interval around every rate forecast widens with it. This is uncertainty about uncertainty, and it has no point estimate. It is the strongest case for holding instruments, inflation protection and macro among them, that do better precisely when the rate outlook becomes harder to read.

The honest part: Every scenario number here is a point estimate inside a range that could widen. The verified layer is the J.P. Morgan baseline assumptions; the factor decomposition, the drawdowns and the spectrum are model estimates. We would rather show the range and the assumptions than a single confident figure that the next Fed press conference could undo. The discipline is not predicting the rate path. It is making sure a portfolio is not relying on a number that says rates are 2% of its risk, when the drawdown says they are 14%.

The reference portfolio carries no special mandate, which is the point: the low rate-factor weight and the thin hedge budget are the default state of a great many growth portfolios that have never been put through a factor and scenario lens. The lesson is portable on both sides of the table. If you allocate, count your risk, not your line items. If you manage money for these allocators, the same analysis is a conversation you can open with evidence: here is the rate exposure your client's model is hiding, and here is the cheapest way to close it.

One honest note: every factor, scenario and rate-sensitivity figure in this analysis is a model estimate, not a forecast. The reallocation's resilience holds on standard scenario grounds; the figures would shift under a different rate path. The J.P. Morgan baseline assumptions are verified against our own data; the model outputs are estimates.

Sources: J.P. Morgan 2026 Long-Term Capital Market Assumptions (10-year, USD), verified against Three Horizons Capital's analytics estate; Three Horizons Capital portfolio analytics, three-factor model and scenario engine; macro backdrop (June 2026 FOMC; May 2026 CPI) corroborated against public reporting as of 25 June 2026. The reference portfolio is analytically constructed and not based on any client's holdings. Three Horizons Capital is not affiliated with J.P. Morgan Asset Management. For research and platform-demonstration purposes; not investment advice.