Take an ordinary, sensible portfolio. Sixty percent in global equity across US, international, emerging and small-cap. Bonds. A little private equity and hedge funds. Some real estate and infrastructure. Cash. Eleven holdings, four asset groups, no obvious concentration. The kind of allocation a thousand family offices and wealth portfolios run today. This is what happened when we ran it through a factor model, and what a disciplined reallocation does about it, with the cost disclosed in full.

A word on the data: portfolio analytics are computed on JPMorgan's 2026 Long-Term Capital Market Assumptions (USD). We verified the six asset-class returns this analysis turns on against our own JPM LTCMA data, and they match to the basis point. The geopolitical overlay and all scenario results are model-derived estimates, labelled as such throughout. The reference portfolio is analytically constructed, with no regional or strategy mandate, and is not based on any client's holdings. For research and platform-demonstration purposes; not investment advice.

01 · The hidden bet

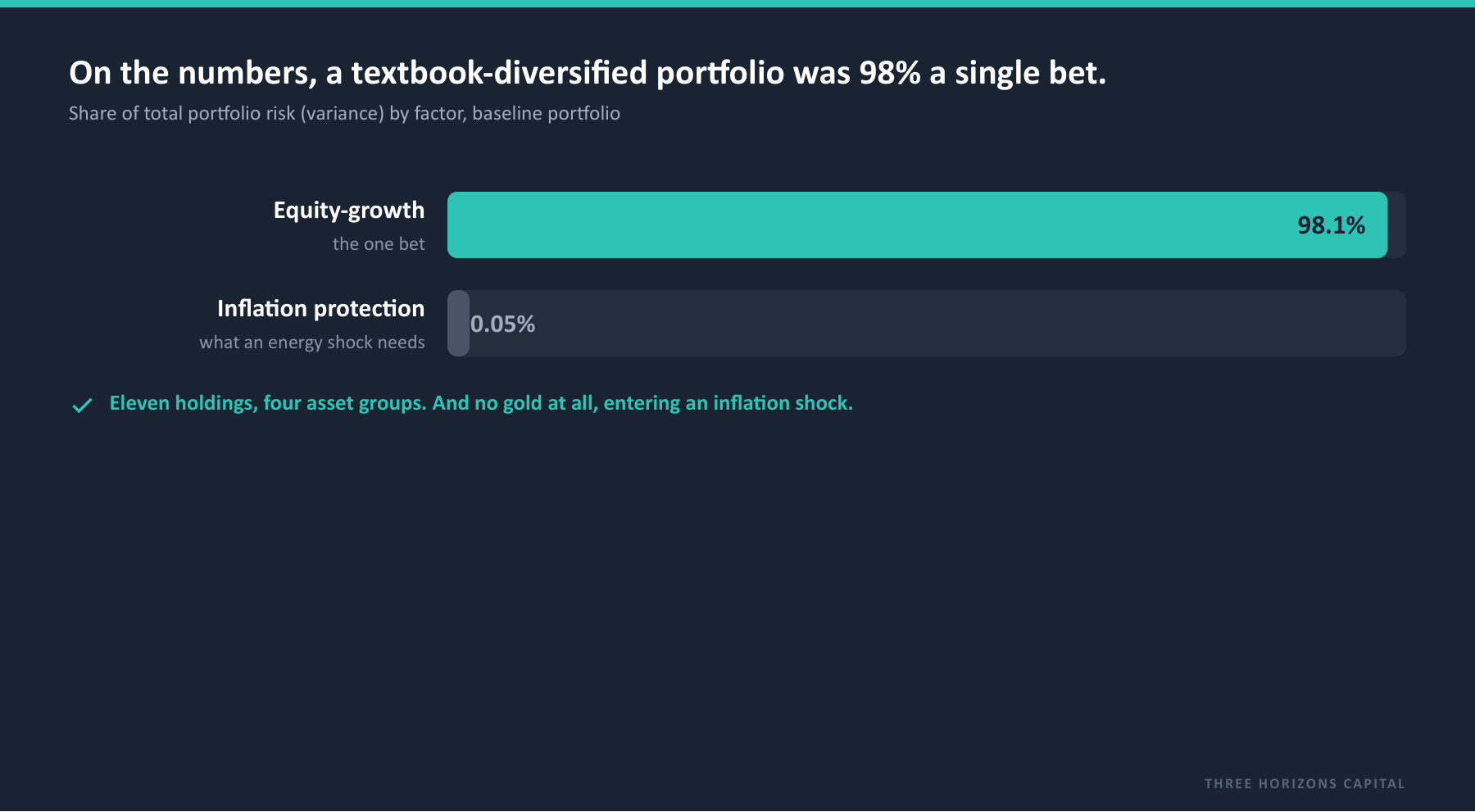

Eleven holdings behaved as one risk.

On paper, a spread across four asset groups. Under a factor lens, the diversification is largely cosmetic. 98.1% of the portfolio's variance loads on a single factor: equity growth. Stripped of labels, it is one large equity position with thin layers around it. The factor that protects a portfolio when inflation runs accounts for 0.05%. There is no gold and no inflation hedge of any kind.

What this tells you: This is a structural observation, not a geopolitical one, and it was true before the first missile flew. Two equity positions alone, US Large Cap and AC World, account for roughly 65% of all portfolio risk. A book that looks diversified by line item is, by risk, a single bet. The book that has never been put through a factor and scenario lens is the one most likely to be one.

02 · The regime and the exposure

The regime that arrived is the one this portfolio cannot absorb.

The 2026 Middle East conflict did its real economic damage through the Strait of Hormuz, which carries roughly a fifth of the world's oil and remains effectively closed. The IEA called it the most significant supply shock in the history of the oil market, which points to one regime above all: persistent, energy-driven inflation and higher-for-longer rates. Mapped against that regime, the exposed positions are not exotic. They are the safe-sounding core.

Conventional bonds, 20% of the book — the clearest negative channel

Duration is the most direct casualty of energy-inflation persistence. As the Federal Reserve loses room to cut, the aggregate-bond and high-yield positions carry the portfolio's sharpest negative transmission.

Core real estate, and nothing on the other side

Rate persistence keeps cap rates under pressure and delays normalisation. And with no gold and a near-zero inflation factor, the portfolio holds no asset positioned to gain from the very shock now defining the regime.

A portfolio entering an inflationary, conflict-driven regime with almost no inflation protection is mispositioned for it, independent of any view on where any single market goes next.

03 · The fix

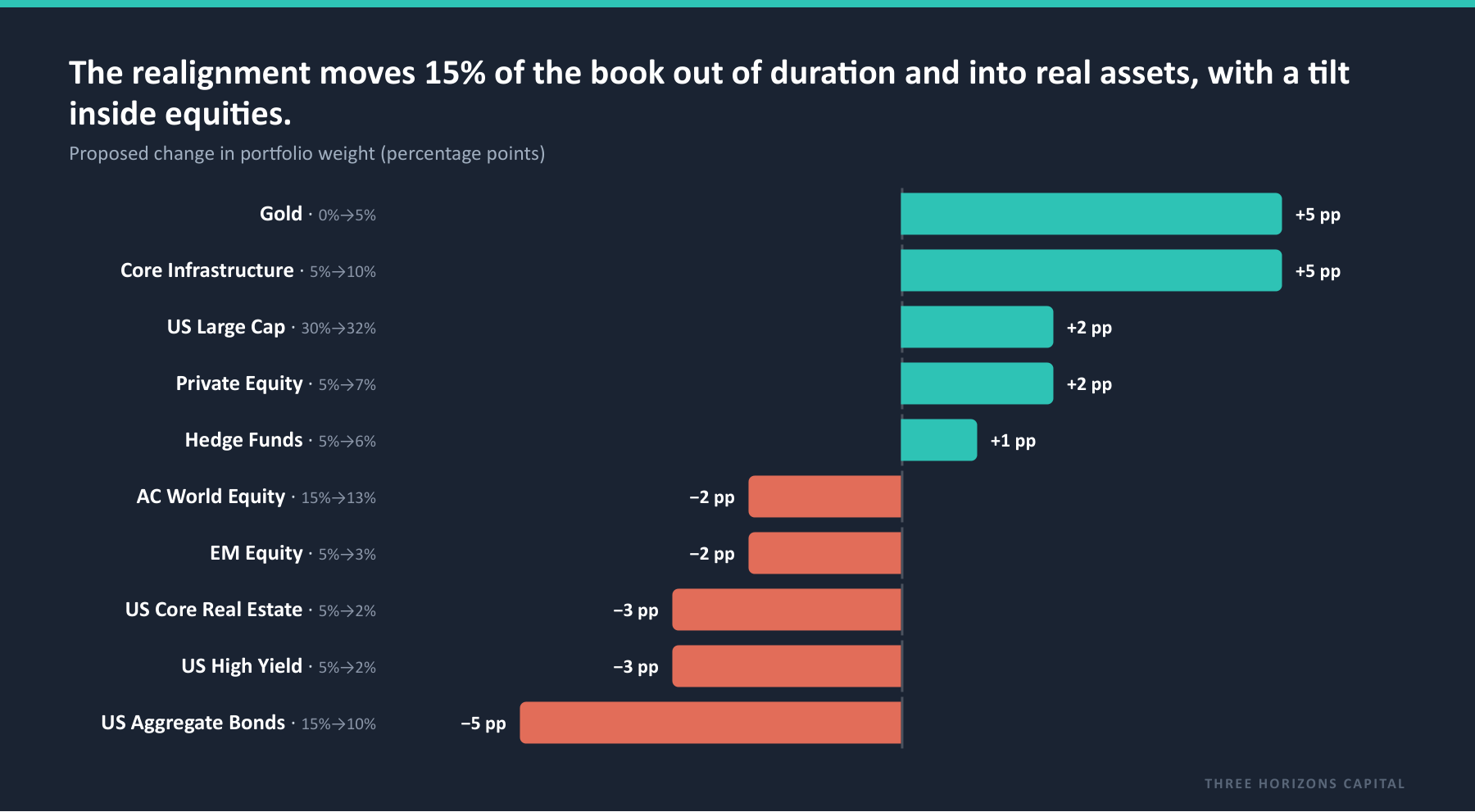

Re-diversify the risk budget, without giving up risk-adjusted return.

The fix is not a dramatic de-risking. It moves fifteen percentage points out of the positions the regime works against and into the ones it favours, with a tilt inside equities, while keeping the portfolio's growth orientation intact.

Each addition has a real claim on the regime: gold as the war-risk and inflation hedge with near-zero equity correlation, infrastructure as the energy-security capex cycle with contracted, inflation-linked cashflows, and private equity as a longer-horizon, structural play on the same themes, defence, critical minerals and reshoring, with its 2026 vintage an attractive entry point. We are honest about the sequencing: the immediate protection comes from gold, liquid today, with the cash buffer held at 5%; private equity draws down over years and earns its place on the long-run view, not as a hedge against this quarter's shock.

What this tells you: On JPMorgan's long-run assumptions the realignment is essentially return-neutral (the displayed return moves about 5bps) and the portfolio's volatility barely changes (11.28% to 11.29%). On the correct, arithmetic Sharpe basis it is in fact a marginal improvement (0.384 to 0.390). It does not cost risk-adjusted return to make; the geopolitical upside sits on top and is the conditional part.

04 · The result, honestly

Resilience first, geopolitics as upside.

Because the trade gives up no risk-adjusted return on the long-run view, the case for it does not need a geopolitical forecast to stand up. It rests on how the portfolio behaves under stress, and there the realignment wins in five of six standard scenarios, with the largest gains exactly where the original portfolio was most exposed.

These improvements are mechanical, not view-dependent: the bond-shock gain comes from cutting duration, the stagflation gain from introducing inflation hedges where there were none, the conflict gain from gold and infrastructure, and the largest of all, in a 2009-style hard recession (+330bps), from stripping out the correlated credit and real-estate risk. They hold in the standard scenario framework regardless of what you believe about the Strait of Hormuz.

The honest part: The geopolitical view is upside layered on top, and we label it an estimate. If our six conflict-driven return adjustments prove directionally right, the realignment earns an additional 39 basis points of expected return (and lifts the geo-adjusted Sharpe from 0.399 to 0.438). That number is conditional; a smooth de-escalation would unwind part of gold's war premium and trim it. The resilience does not depend on it; the extra return does. An allocator does not need a free-lunch promise. They need to see, separately, what is structural and what is a view, and be told which is which.

05 · What this means

The portfolio is ordinary on purpose. So is the blind spot.

The deepest change is in the shape of the risk, not the headline return. The portfolio gains a real inflation hedge where it had effectively none. We will not oversell the factor-variance figure, which barely moves, from 0.05% to 0.33% of variance, because in a book that is 98% equity that share is the wrong lens: equity risk swamps everything, so even a genuine hedge hardly registers as a share of variance. The honest evidence that the hedge works is the stress test, where the realignment gains 160 basis points in the stagflation scenario. The reference portfolio carries no special mandate and no regional tilt, which is the point: the single-factor concentration and the absence of inflation protection are the default state of a great many growth portfolios that have never been put through a factor and scenario lens.

So the lesson is portable on both sides of the table. If you allocate, count your risk, not your line items, because the diversified-looking book is the one most likely to be a single bet in disguise. If you manage money for these allocators, the same analysis is a conversation you can open with evidence: here is where your client is concentrated, here is the hedge they are missing, and here is a correction that gives up no risk-adjusted return on the long-run numbers.

That is the whole capability in one sentence: take any portfolio, ground it in reconciled capital-market assumptions, decompose its real risk, and show, with the cost disclosed, how to make it behave better when it matters most.

One honest note: every geopolitically-adjusted return and scenario result in this analysis is a model estimate, not a forecast. The realignment's resilience holds on long-run scenario grounds alone; the +39bps of geo-adjusted return is conditional on the stated views and would weaken under a rapid de-escalation. The baseline JPM LTCMA figures are verified; the overlay is a scenario. Sharpe ratios are computed on an arithmetic-return basis (the standard mean-variance convention). Private equity, real estate and infrastructure use standard, unadjusted capital-market assumptions; appraisal smoothing can understate private-asset volatility, but the figures here already assign private equity a volatility near 20%, and the +2pp private-equity position sits above the portfolio's own volatility, so it adds rather than suppresses risk, and is included as a long-horizon structural play, not a liquid hedge.

Sources: JPMorgan 2026 Long-Term Capital Market Assumptions (USD), verified against Three Horizons Capital's analytics estate; JPMorgan standard stress-scenario shocks; Three Horizons Capital portfolio analytics and three-factor model; geopolitical and energy detail from publicly available information as of 25 June 2026. The reference portfolio is analytically constructed and not based on any client's holdings. Three Horizons Capital is not affiliated with J.P. Morgan Asset Management. For research and platform-demonstration purposes; not investment advice.